Oreb Market Update April 2026

Friday, May 8, 2026

Market Overview

Ottawa’s housing market continued its seasonal rebound in April, with activity picking up

month-over-month, following a slower winter. Inventory levels, which have been rising since

late summer 2025, remain elevated but stable. The spring increase in new listings has added to

this supply, giving buyers more choice and flexibility.

The broader economic backdrop remains mixed. The Canadian Real Estate Association

(CREA) recently revised its 2026 forecast downward, citing a weaker-than-expected start to the

year and renewed inflation pressures, partly driven by rising energy costs. As a result,

expectations for both sales and price growth have been tempered, with only modest gains now

anticipated nationally.

Interest rate expectations have shifted. Earlier concerns that inflation could lead to rate

increases contributed to more cautious buyer behaviour over the winter. With rates now holding

steady, that immediate risk has eased. While borrowing costs remain above pandemic-era

lows, they are more in line with long-term norms. A more stable rate environment may help

reduce hesitation and support a gradual improvement in activity as buyer confidence

strengthens.

“We’re seeing the market find its footing after a slower winter,” said OREB President Tami

Eades. “April’s activity reflects a market that is gradually regaining momentum. Buyers are

beginning to re-engage, and more listings are helping to keep conditions balanced across most

segments.”

Residential Market Activity

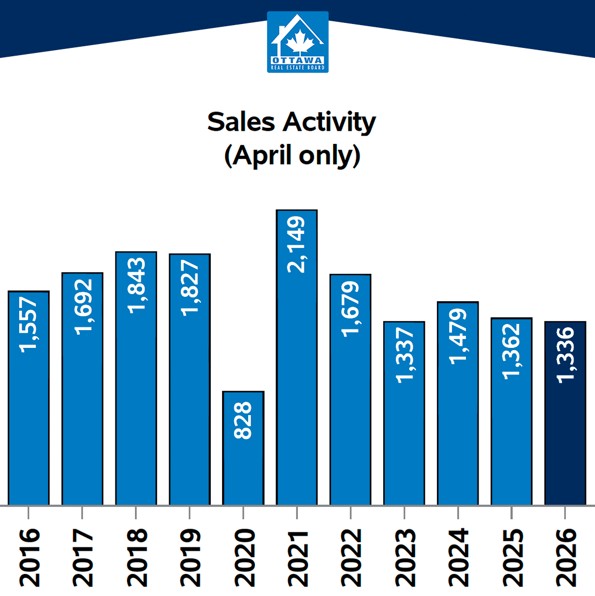

In April, 1,336 homes were sold, down 1.9% year over year, but up from 1,075 in March.

New listings rose sharply to 3,258 units (+19.3%), pushing active listings to 4,535 units

(+17.2%).

With listings continuing to outpace sales, the sales-to-new-listings ratio came in at 41.0%,

consistent with balanced market conditions. Homes are taking slightly longer to sell, with

median days on market increasing to 21 days, up from 18 days in April 2025.

Year to date, 3,839 homes have been sold, down 4.4% compared to the same period in 2025.

While activity remains below last year’s levels, recent trends suggest that the 2026 market may

be gradually strengthening.

New listings total 8,933 units (+8.5%), while active listings have increased 16.0%.

Prices and Market Balance

Home prices held steady in April. The average sale price was $712,184 (+0.8% year over

year), and the median price was $650,000, unchanged from April 2025. Year-to-date, the

average price stands at $683,303, and the median price is $630,000, both showing little change

compared to the same period last year.

The MLS® Home Price Index provides additional context, indicating that benchmark prices

have begun to stabilize following earlier declines. Most segments recorded modest month-over-

month gains, apart from condo-apartments, which continue to lag. This aligns with the broader

trend of price stabilization observed over recent months.

? Single Family: 3.1

? Townhome: 3.0

? Apartment: 4.9

Regional Market Comparison

Market conditions across Ottawa’s subareas continue to vary.

Ottawa Centre appears relatively stable from a pricing standpoint, but activity has eased. Sales

are lower compared to recent years, while inventory has increased, resulting in slower

absorption. This is largely due to the area’s higher concentration of condo-apartment units,

which has been the softest segment of Ottawa’s market for several months.

Suburban markets across the east, south, and west remain generally balanced. Sales-to-new-

listings ratios and inventory levels are within typical historical ranges, although sales activity

has moderated in some areas and supply has trended higher. Among these, the western

suburbs stand out as the strongest segment, with more consistent sales activity and slightly

tighter inventory conditions.

Rural markets continue to operate at a slower pace, with higher inventory levels and longer

selling times compared to suburban areas. This results in more buyer-friendly conditions, along

with greater variability in pricing data due to lower transaction totals.

Overall, while Ottawa’s market remains balanced at a high level, local conditions vary.

Suburban areas are the most stable, with the west currently leading in activity. Central areas

are seeing more moderate demand, while rural markets continue to experience slower

absorption, contributing to a more varied regional landscape. Those interested in exploring

these dynamics further can access the non-HPI report in the monthly stats package here.